Take a closer look at some of the fundamentals underlying the recent positive economic news.

In its monthly "beige book" report, the Federal Reserve recently reported moderate economic growth across the country. This was backed up by gross domestic product numbers, which showed a 2.5 percent annualized growth in the first quarter--a significant improvement from the 0.4 percent annualized growth from the fourth quarter of 2012. The unemployment rate continues to tick down. Personal income and spending both increased, pending home sales reached a three-year high, new residential home sales improved, and home prices are surging. The American auto industry had its best performance in 20 years. Most economic indicators seem to be in the normal range.

But--hold on a minute. A recent report found that U.S. home ownership fell to its lowest level since 1995. Both manufacturing activity in the country and orders for durable goods plunged last month. A Kauffman report revealed that entrepreneurial activity declined last year, and the National Federation of Independent Businesses said last month that small business confidence remains at historically low levels. If that's not bad enough, the University of Michigan said that consumer sentiment fell to a three-month low, and, separately, port traffic in the Los Angeles area decreased in March. Things are so gloomy that more than 12 million Americans actually believe that lizard people are running the country.

So is the economy in good shape--or not?

Why are so many small business owners still not feeling as confident as they did a few years ago? The fact is that most of the business people I speak with are very tentative, still uncertain, and still very concerned about some of the fundamentals underlying the numbers.

Here's four reasons why:

1. A deficit decline is not sustainable.

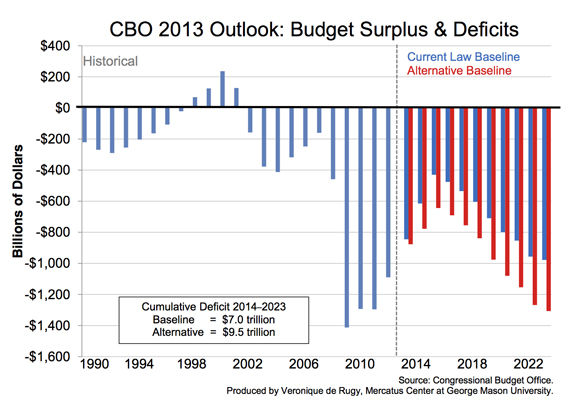

Since 2009 the country has become accustomed to a trillion-dollar annual deficit. I've been watching, with a growing sense of panic, the U.S. national debt, which is now approaching $17 trillion and is, for the first time in U.S. history, greater than the entire national output. But some are celebrating. That's because many projections now show that, with rising tax receipts and some cuts in government spending, the deficit this year is projected to fall to under $800 billion. And the projected annual deficit is estimated will decrease to as little (as little?) as $600 billion by 2015. This doesn't mean the deficit is under control, and you know it. Back in 2007, the deficit was "only" $161 billion and even that was too high. Remember, this is all adding to the country's national debt. And after 2015, the deficit is projected to increase yet again, soon surpassing a trillion dollars a year as the costs of health care, social security, and other entitlements begin kicking in with a vengeance. The business owners I know aren't buying into the myth that the deficit is coming down. The long-term debt could affect the U.S. economy as it's now doing in parts of Europe: rising interest, cuts in spending, tax increases, exchange rate fluctuations, economic turmoil. A decrease in the deficit is purely a short-term thing. I'm concerned about the long term.

{kind=link}

2. The stock market boom does not indicate a strong economy.

No one is complaining about the recent rise in stock prices. The benefits of a strong stock market are enormous for small business: It gives customers confidence to spend, adds to a general feeling of optimism in the market, and sure feels good to see my own investment accounts going up, particularly since I have college tuition bills looming. But many business owners I know have serious doubts about the strength of the stock market. Why? Because with easy money flooding the market from the Fed, interest rates so low, and real estate barely recovering, where else is there to invest but the stock market? It's pretty much the only choice for someone not willing to take an enormous amount of speculative risk. So the money flows to the stock market, and prices go up. Does this mean that the market's growth is truly indicative of a strong economy? Or is it a temporary phenomenon? I'm wary, and trying to limit my exposure.

3. Inflation is not dead.

I have to give credit where credit is due: the Federal Reserve has managed to keep inflation pretty much under control for the past 25 years. This has helped keep U.S. prices competitive, costs under control, and interest rate risk at a reasonable level. But if you dig into this, like I did, you get concerned. As shown here, the Fed's balance sheet has literally exploded over the past few years because of the Troubled Asset Relief Program (TARP) and bond purchases. These initiatives were done with good reason--to provide liquidity to struggling markets. But what if the economy grows more than expected? What if the demand for new loans substantially increases, and excess reserves are drawn down by banks eager to fill the needs of their customers at a rate that's faster than the Fed can control? What if the Fed's exit strategy isn't effective? It's a very high risk game and, if mistakes are made, inflation, followed by high interest rates, could very well happen. Inflation is not dead. It's a dangerous animal that is, for now, kept in its cage. I'd bet you're watching and hoping that this cage holds like I am.

{kind=link}

4. Corporations don't have as much cash as it seems.

There's no doubt that companies have a lot of cash on hand. In fact, recent numbers show that non-financial companies have about $2.3 trillion in their bank accounts, a historical high. But this number is misleading. As financial analyst James Bianco explained in this great column: "Liquid assets held on companies' balance sheets is a nominal number, much like the nominal level of GDP, that rarely decreases. Of course cash on the sidelines is at a record nominal level; it usually is. This series must be compared to other balance sheet items for relevance." He uses a chart to explain it: In 1952, 40 percent of companies' total assets were "liquid assets" (cash), and that number is down to only 15 percent today. "It is not as though companies currently have 40 percent of their assets in the form of cash waiting to be invested, as was the case in the 1950s," says Bianco. If investment opportunities become more "enticing," and companies see a potential to make a profit, these levels will drop to the 30-year historical norm of 10 percent or 11 percent.

These are concerns. But no reason to panic. There are always concerns. And one great thing about being a business owner is that you're a glass-is-half-full person. The country is at the very beginning cusp of an energy boom, has tremendous technological resources, a market full of skilled people, and a free economy that is enjoying low interest and low inflation. Of course there are challenges, but no matter how much I complain, there is not a single business owner I speak to who would prefer to be living, raising her children, and doing business anywhere else but in the United States. And that speaks for itself.

|

No comments:

Post a Comment